Article and Commentary: Lessons in Precision from a Three Minute Board Meeting

Listen to the exciting Board of Assessors Meeting on any device, CLICK PLAY.

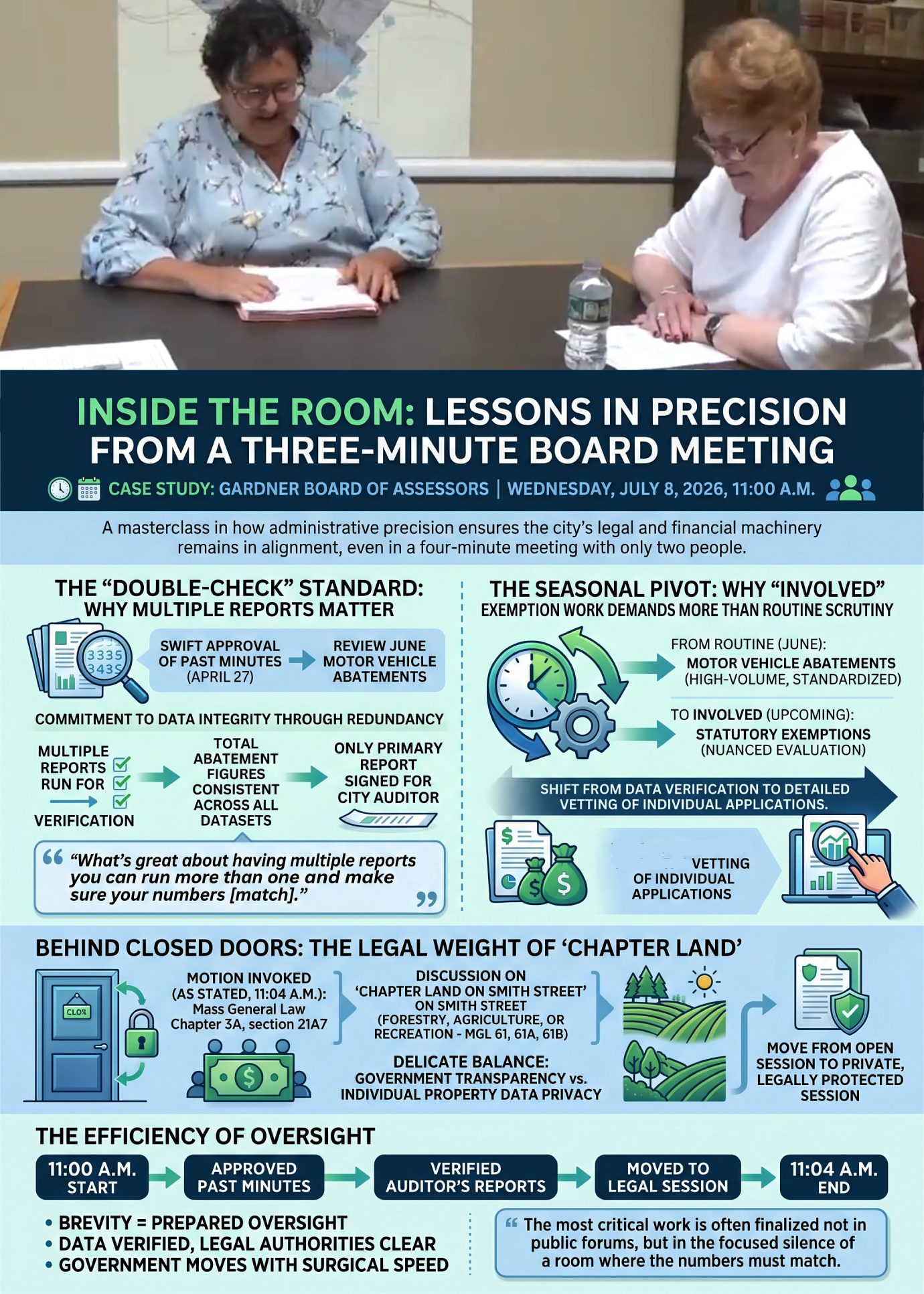

While public attention is often captured by the high-drama debates of city councils or state legislatures, the foundational work of a municipality happens in much quieter, leaner settings. On Wednesday, July 8, 2026, the Gardner Board of Assessors convened at 11:00 a.m. for a meeting that lasted under three minutes. In a room occupied by only two people—a stark reminder of the lean efficiency often required in local administration—the board moved through a series of actions that underscored the meticulous nature of municipal finance and law.

This session was not merely a formality; it was a masterclass in how administrative precision ensures the city’s legal and financial machinery remains in perfect alignment.

The “Double-Check” Standard: Why Multiple Reports Matter

The meeting opened with the swift approval of the minutes from April 27, 2026, before transitioning into a review of the June 2026 motor vehicle abatements. To the uninitiated, signing off on tax abatements might seem like a clerical footnote. However, the board’s workflow reveals a sophisticated commitment to data integrity through redundancy.

The board reviewed multiple reports to ensure that the total abatement figures were consistent across all datasets. This process is not just for internal peace of mind; it is a critical intersection between the Assessors and the City Auditor. The board specifically noted that while multiple reports are run for verification, not every copy requires a signature—only the primary report destined for the Auditor’s office. This ensures a clean paper trail for the city’s financial oversight while maintaining a secondary “check” system to prevent clerical errors before they reach the general ledger.

“What’s great about having multiple reports you can run more than one and make sure your numbers [match].”

The Seasonal Pivot: Why ‘Involved’ Exemption Work Demands More Than Routine Scrutiny

Municipal governance is a cyclical endeavor, and this July meeting marked a clear transition point in the fiscal calendar. As the board finalized the routine motor vehicle abatements from the previous month, they prepared for the shift toward more complex territory: statutory exemptions.

While motor vehicle abatements are often high-volume and standardized, the upcoming focus on exemptions represents a more “involved” phase of work. For the board, this means a shift from data verification to the nuanced evaluation of individual applications. This seasonal pivot requires a higher level of scrutiny, as exemptions directly impact the city’s tax base and require strict adherence to eligibility criteria. The transition from the “routine” to the “involved” is where the expertise of the board is most tested, moving from broad oversight to the detailed vetting of personal and financial qualifications.

Behind Closed Doors: The Legal Weight of “Chapter Land”

As the clock neared 11:04 a.m., the board moved into an executive session, a transition that highlights the delicate balance between government transparency and the privacy of individual property data. Invoking the motion as stated—under Mass General Law Chapter 3A, section 21A7—the board shifted focus to a specific discussion regarding “Chapter land on Smith Street.”

From an analyst’s perspective, the mention of “Chapter land” refers to properties classified under MGL Chapters 61, 61A, or 61B. These laws provide tax incentives for land used for forestry, agriculture, or recreation. Because discussions regarding these classifications often involve sensitive financial data, usage commitments, and personal property details, the law mandates a move from open session to a private, legally protected session. By adjourning the open meeting to address the Smith Street property in executive session, the board demonstrated a disciplined adherence to the legal protocols that protect both the taxpayer’s privacy and the city’s statutory obligations.

The Efficiency of Oversight

The transition from the public review of abatements to the private scrutiny of land use was handled with the same brisk efficiency that defined the start of the meeting. By 11:04 a.m., the Gardner Board of Assessors had approved past minutes, verified the Auditor’s abatement reports, and moved into a legally mandated session for sensitive land classification.

This brevity is not a sign of a lack of depth; rather, it is the byproduct of prepared oversight. When the data is verified and the legal authorities are clearly understood, the machinery of government can move with surgical speed. It prompts a vital question for the modern citizen: How often do we consider the administrative precision and the quiet, three-minute increments of labor required to keep our own cities running smoothly? The most critical work of a municipality is often finalized not in the heat of a public forum, but in the focused silence of a room where the numbers must always match. Kudos to Assessor Christine Kumar and member Paulette Burns for their diligent work.