AM FM Radio – Still on Top – Reports by Gardner Magazine

Listen to a “Deep Dive” podcast on why Automakers Can’t Kill AM Radio – It’s important to the public.

Listen to this “Debate” podcast on radio.

Jump to various sections on this page: Enduring Dominance of AM/FM Radio in the Automotive Landscape. —- Analysis of Listening by Demographics and Manufacturer — The Dashboard Rebellion: Why the Future of the Car is Unexpectedly Analog —-Fact Sheet: The American Dashboard—Modern vs. Traditional Audio Habits —- Market Analysis Report: The In-Vehicle Audio Landscape and the Strategic Primacy of AM/FM Radio

Watch the following short video.

The Enduring Dominance of AM/FM Radio in the Automotive Landscape

The Enduring Dominance of AM/FM Radio in the Automotive Landscape

The following report synthesizes recent market research and industry data regarding the status of AM/FM radio in the United States automotive sector. Despite the proliferation of digital streaming services and satellite radio, AM/FM radio remains the primary audio source for American drivers.

Critical Takeaways:

- Universal Demand: 96% of Americans view built-in AM/FM radio as an essential feature in new vehicles, with 89% stating they would likely decline to purchase a car lacking over-the-air radio.

- Market Dominance: AM/FM radio accounts for approximately 54% to 60% of all in-car listening time. Its dominance is even more pronounced in the ad-supported sector, where it captures an 83% to 86% share.

- Safety Imperative: 90% of consumers view radio as vital for emergencies. AM radio, in particular, serves as the backbone of the Emergency Alert System (EAS), maintaining functionality when cellular and internet networks fail.

- Demographic Resilience: While digital native demographics (ages 13–34) show higher streaming usage, nearly half of their in-car listening time still belongs to terrestrial radio.

- Legislative Pressure: In response to automakers—specifically Tesla and Rivian—removing AM tuners, the “AM Radio for Every Vehicle Act” has gained bipartisan support from over 340 members of Congress to mandate radio as a standard safety feature.

——————————————————————————–

Consumer Sentiment and Purchase Intent

Research from Critical Mass Insights and Edison Research indicates an overwhelming consumer preference for terrestrial radio as a standard automotive feature. This preference remains consistent even among consumers who do not listen to the radio regularly.

Key Statistics on Consumer Preference

- General Necessity: 96% of Americans want AM/FM radio in their vehicles.

- Free Access: 97% of respondents consider having free entertainment options in their cars essential, largely due to “streaming fatigue” and the costs associated with subscription services.

- Ease of Use: 98% of Americans believe radio should be simple to locate. However, design trends show a decline in physical buttons; only 26% of the 100 best-selling US models feature a physical radio button, down from 36% in 2024.

- Purchasing Deterrence: 89% of consumers report that the absence of a radio would likely prevent them from purchasing a specific vehicle model. This far exceeds earlier studies by Xperi’s DTS, which placed that figure at 62%.

——————————————————————————–

Market Share and In-Car Listening Trends

Data from Edison Research’s “Share of Ear” study (Q2 2025 and Q1 2026) confirms that AM/FM radio remains the leader in the “battle for the dashboard.”

Total In-Car Audio Time Spent

Across all audio types—including ad-free subscriptions—AM/FM radio holds a commanding lead over its competitors.

| Audio Platform | Share of Total In-Car Listening |

|---|---|

| AM/FM Radio | 54% – 60% |

| SiriusXM (Ad-free) | 10% – 15% |

| Streaming Music (Spotify, Apple, etc.) | 15% – 16% |

| Podcasts | 8% – 12% |

Dominance in Ad-Supported Audio

For advertisers, the automotive environment is a critical “path to purchase.” AM/FM radio represents the vast majority of ad-supported audio time in vehicles.

- Overall Ad-Supported Share: 83% to 86%.

- Comparison to Rivals: AM/FM’s 83% share dwarfs competitors like podcasts (8%), ad-supported SiriusXM (4%), and ad-supported Spotify (3%).

Post-Pandemic Rebound

The proportion of total AM/FM radio listening that occurs in vehicles has returned to pre-pandemic norms. In 2025, 53% of all AM/FM tuning occurred in cars, up from a low of 40% during the peak of the pandemic (2021–2022). Over the last decade, in-car listening’s share of total radio usage has grown by 25%.

——————————————————————————–

Analysis of Listening by Demographics and Manufacturer

Analysis of Listening by Demographics and Manufacturer

Demographic Breakdown

The data challenges the assumption that younger generations have completely abandoned terrestrial radio.

- Ages 13–34: AM/FM radio accounts for 46% of in-car listening, while streaming music has grown to 30%.

- Ages 18–34: This group still devotes 77% of their ad-supported in-car audio time to AM/FM radio.

- Gender: Women show an “astonishingly high” proportion of in-car listening. Among women aged 18–34, 72% of all over-the-air AM/FM radio time is spent in the vehicle.

- Purchasing Power: NPR listeners aged 35+ are 38% more likely to have a household income of $100,000+ and 39% more likely to have spent $1,000+ online in the last six months.

Performance by Vehicle Brand

Listening habits remain remarkably consistent across different automotive manufacturers, even in those that have attempted to phase out traditional tuners.

- General Motors: Leads with 60.7% to 62% of in-car audio time devoted to AM/FM.

- Tesla: Despite the removal of AM tuners in some models and plans to remove FM from base models, Tesla drivers still spend 51% of their audio time listening to AM/FM radio.

- Domestic vs. Import: In-car AM/FM share is nearly identical between domestic drivers (53%) and import drivers (55%).

——————————————————————————–

Public Safety and the Emergency Alert System (EAS)

The primary argument for the preservation of AM radio is its role as a “lifeline” during national or local crises.

- Emergency Reliability: 90% of respondents view radio as vital during severe weather or natural disasters. AM radio has a long range and functions when power is out and cell towers are down or congested.

- Primary Entry Points (PEPs): 77 radio stations (mostly AM) serve as PEPs, covering 90% of the American population. These stations have direct connections to FEMA and the National Weather Service, ensuring authoritative information distribution during grid failures.

- Automaker Vulnerability: Removing over-the-air tuners forces reliance on cellular or internet data, which is vulnerable to network outages and often requires subscription fees.

——————————————————————————–

Industry and Legislative Response

The move by some automakers (Tesla, Rivian, and initially Ford) to remove AM tuners—citing electromagnetic interference from electric vehicle (EV) motors—has met significant resistance.

Legislative Action

The AM Radio for Every Vehicle Act is a bipartisan effort to mandate AM capability as a standard safety feature.

- Support: More than 340 members of the House and Senate support the bill.

- Advocacy: The National Association of Broadcasters (NAB) and the International Association of Fire Chiefs have argued that automakers are prioritizing profits over public safety by removing local radio.

Manufacturer Reversals

Following “massive backlash” from consumers and politicians, Ford Motor Company reversed its decision to remove AM radio from its newer models, demonstrating the significant influence of consumer and legislative pressure on vehicle design.

——————————————————————————–

Conclusion

AM/FM radio is not a legacy technology in decline but a dominant, preferred, and essential medium within the automotive environment. Its resilience is underpinned by its cost-free access, ease of use, local connection, and critical role in public safety. For automakers, removing radio tuners poses a significant risk to brand loyalty and purchase intent. For marketers, the data confirms that the car remains the most effective environment for reaching a captive audience at scale.

——————

The Dashboard Rebellion: Why the Future of the Car is Unexpectedly Analog

The Dashboard Rebellion: Why the Future of the Car is Unexpectedly Analog

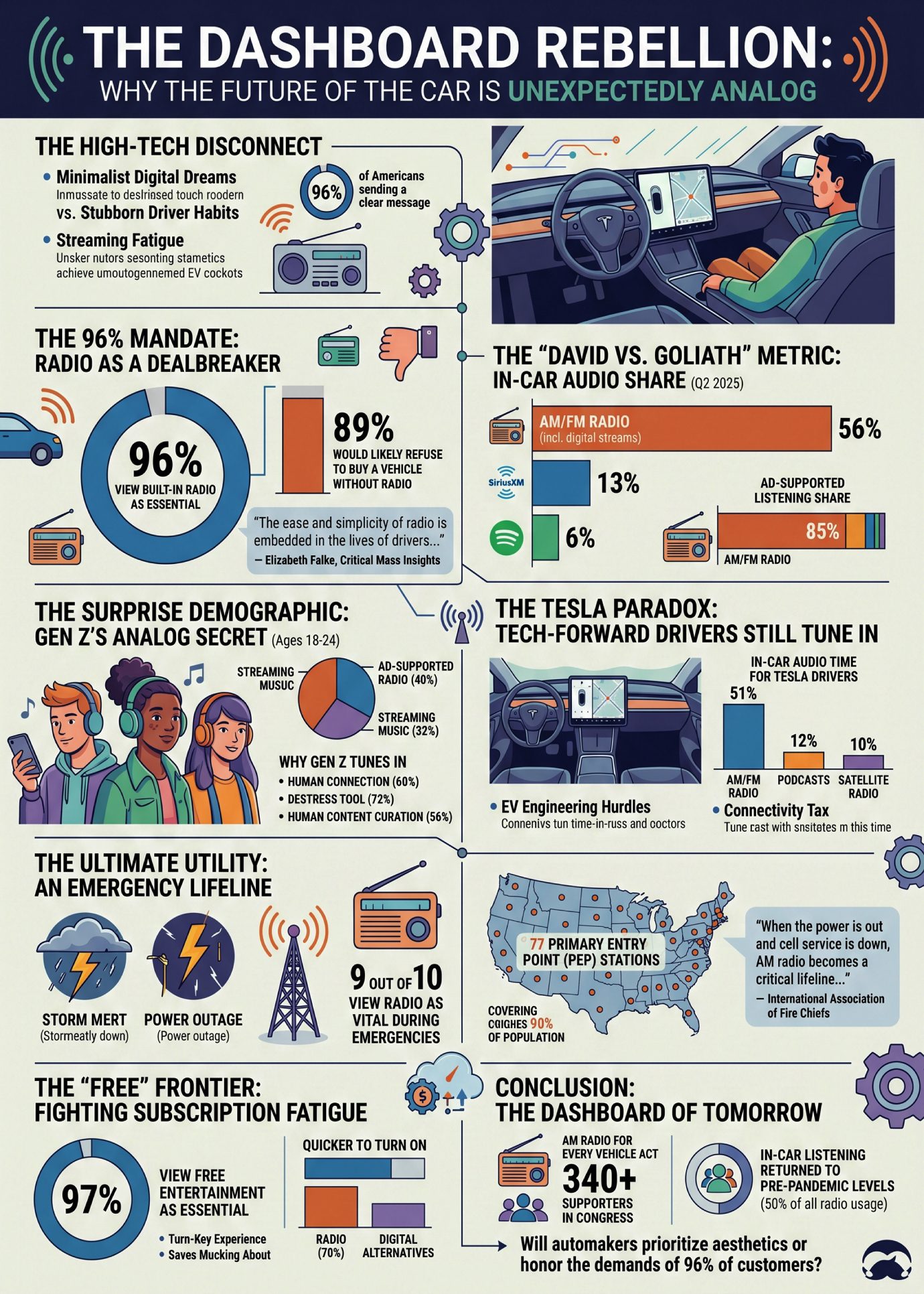

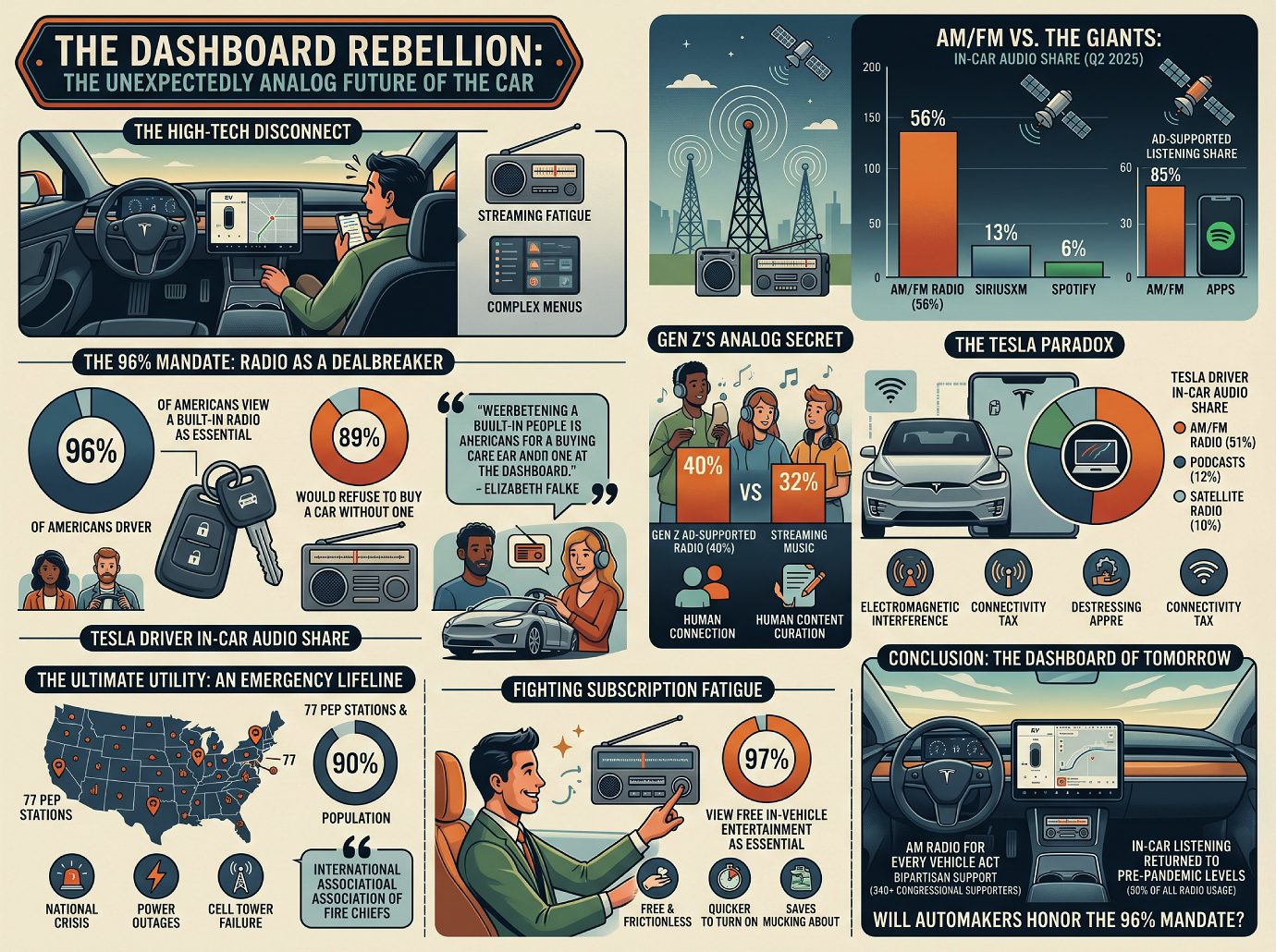

The High-Tech Disconnect

Step into a modern electric vehicle, and you are greeted by a cockpit that feels more like a high-end Silicon Valley boardroom than a traditional automobile. Minimalist glass surfaces and sprawling touchscreens suggest a future where the driver is a consumer of curated, ad-free digital ecosystems. Automakers are betting billions that we want our cars to be giant smartphones on wheels, yet a profound irony has emerged: as dashboards get smarter, drivers are reaching for a technology that hasn’t fundamentally changed in a century.

A massive disconnect exists between the minimalist digital dreams of manufacturers and the stubborn reality of American driver habits. While the industry pushes proprietary apps and subscription-based interfaces, consumers are exhibiting a phenomenon known as “streaming fatigue”—a growing exhaustion with managing endless monthly payments and the cognitive friction of navigating complex menus while traveling at 70 miles per hour. Despite the high-tech push, 96% of Americans are sending a clear message that the future of the car is unexpectedly analog.

The 96% Mandate: Radio as a Dealbreaker

Data from Critical Mass Insights confirms that the inclusion of a radio is no longer just an expected feature; it has become a prerequisite for the automotive purchase. An overwhelming 96% of Americans view a built-in radio as an essential component of a new vehicle. This isn’t merely a preference expressed by older generations; the mandate cuts across every demographic, including those who may not even be daily listeners.

For manufacturers looking to trim costs by removing “legacy” hardware, the consumer response is a stark warning. The study found that 89% of respondents would likely refuse to buy a vehicle if it lacked a built-in radio. In an era where automakers spend hundreds of millions on UI/UX to create a seamless experience, they are finding that the absence of a simple AM/FM tuner is a primary dealbreaker for a multi-thousand-dollar investment.

“The ease and simplicity of radio is embedded in the lives of drivers consuming various forms of audio in their cars. Consumers want radio for a variety of different reasons that are largely unique to local radio—everything from discovering what new music matters to weather updates, the latest sports reports, and local news and events.” — Elizabeth Falke, Senior Vice President of Research for Critical Mass Insights.

The “David vs. Goliath” Metric: AM/FM vs. The Giants

The perceived dominance of streaming giants and satellite platforms often dissipates when filtered through actual in-car usage. According to the Edison Research “Share of Ear” study for Q2 2025, AM/FM radio captures a dominant 56% share of all in-car audio time. This figure is inclusive of digital streams of AM/FM stations, proving that “radio” is a resilient content category that is successfully migrating to digital platforms rather than being replaced by them. This 56% share stands in sharp contrast to the 13% share held by SiriusXM and the mere 6% share owned by Spotify.

The lead becomes even more pronounced when analyzing the market through the lens of advertising. For ad-supported listening, the AM/FM share jumps to an unmatched 85%. In an age of sophisticated algorithms, the simple broadcast signal remains the “queen of the road,” providing a mass reach that digital-only platforms have yet to replicate.

The Surprise Demographic: Gen Z’s Analog Secret

The most counter-intuitive defenders of the radio dial are Gen Z. Often dismissed as digital natives who only exist within the silos of TikTok or Spotify, listeners aged 18 to 24 are showing a distinct affinity for broadcast media. Key data shows that Gen Z consumes more ad-supported radio (40%) than streaming music (32%).

The draw for this demographic is deeply psychological. While algorithms provide precision, they often lack the “human connection” of a live personality. Approximately 60% of Gen Z listeners report that tuning in feels like “hanging out” with the hosts, and 72% use the radio specifically as a tool to destress. Most importantly, 56% of Gen Z prefer radio’s human content curation over digital-only platforms. For a generation saturated in automated suggestions, the presence of a live person choosing the next track offers a sense of companionship and discovery that a cold code cannot provide.

The Tesla Paradox: Tech-Forward Drivers Still Tune In

Tesla has led the charge in phasing out traditional AM hardware, citing a specific engineering hurdle: electromagnetic interference from electric motors. To avoid the billions of dollars required to shield AM reception from the car’s own propulsion system, several EV manufacturers have simply deleted the tuner. This essentially forces a “connectivity tax” on drivers, pushing them toward data-hungry streaming alternatives.

Yet, Tesla owners are resisting this digital migration. Despite the hardware being intentionally sidelined, AM/FM radio still accounts for 51% of all in-car audio time for Tesla drivers. This usage significantly beats out podcasts (12%) and satellite radio (10%). Even in the most technologically aggressive segment of the market, the consumer’s first instinct is to find a way back to the broadcast signal, highlighting the enduring role of radio even when the dashboard tries to kill it.

The Ultimate Utility: An Emergency Lifeline

Beyond entertainment, the radio serves as the nation’s ultimate utility. In the event of a national crisis or local disaster, cellular networks and 5G internet are notoriously fragile. When power grids fail or cell towers become overloaded, the broadcast signal remains the only reliable link between the government and the public.

This is why 9 out of 10 respondents view radio access as vital during emergencies. The technical infrastructure supporting this is immense: there are 77 Primary Entry Point (PEP) stations across the U.S. that are specifically hardened to survive disasters. These stations cover 90% of the American population, providing a direct, unhackable connection to FEMA and the National Weather Service.

“When the power is out and cell service is down, AM radio becomes a critical lifeline. Its long range and ability to operate during power outages, natural disasters and extreme weather events make it an indispensable resource for those in desperate need of reliable updates.” — International Association of Fire Chiefs.

The “Free” Frontier: Fighting Subscription Fatigue

As modern life becomes a series of endless monthly charges, the appeal of free, frictionless content is reaching a breaking point. Research shows that 97% of Americans view free entertainment options in their vehicles as essential. Radio offers a “turn-key” experience that high-tech interfaces struggle to match; 70% of younger listeners prefer radio because it is “quicker to turn on” than digital alternatives.

The sophistication of a “smart” dashboard often results in a poor user experience. As one consumer succinctly put it in recent commentary, radio is simply preferred because it “saves mucking about” with phone connections and app navigation. In an age of “streaming fatigue,” the ability to simply hit a button and receive high-quality, localized content for free remains a primary driver of consumer satisfaction.

Conclusion: The Dashboard of Tomorrow

The tension between automaker minimalism and consumer reality has finally moved from the dealership to the halls of government. The “AM Radio for Every Vehicle Act” has gained massive bipartisan support—garnering more than 340 supporters in Congress—as lawmakers seek to mandate the technology as a standard safety feature. This legislative push reflects a broader cultural rebound: in-car listening has now returned to pre-pandemic levels, accounting for 50% of all radio usage.

As we look toward the dashboard of tomorrow, the industry faces a fundamental choice. Will automakers continue to prioritize minimalist digital aesthetics and subscription revenue, or will they honor the explicit demands of the 96% of their customers who want their analog lifeline to stay? The data suggests that if manufacturers continue to ignore the human desire for free, local, and reliable connection, they may find themselves manufacturing a future that no one is willing to buy. ———————–

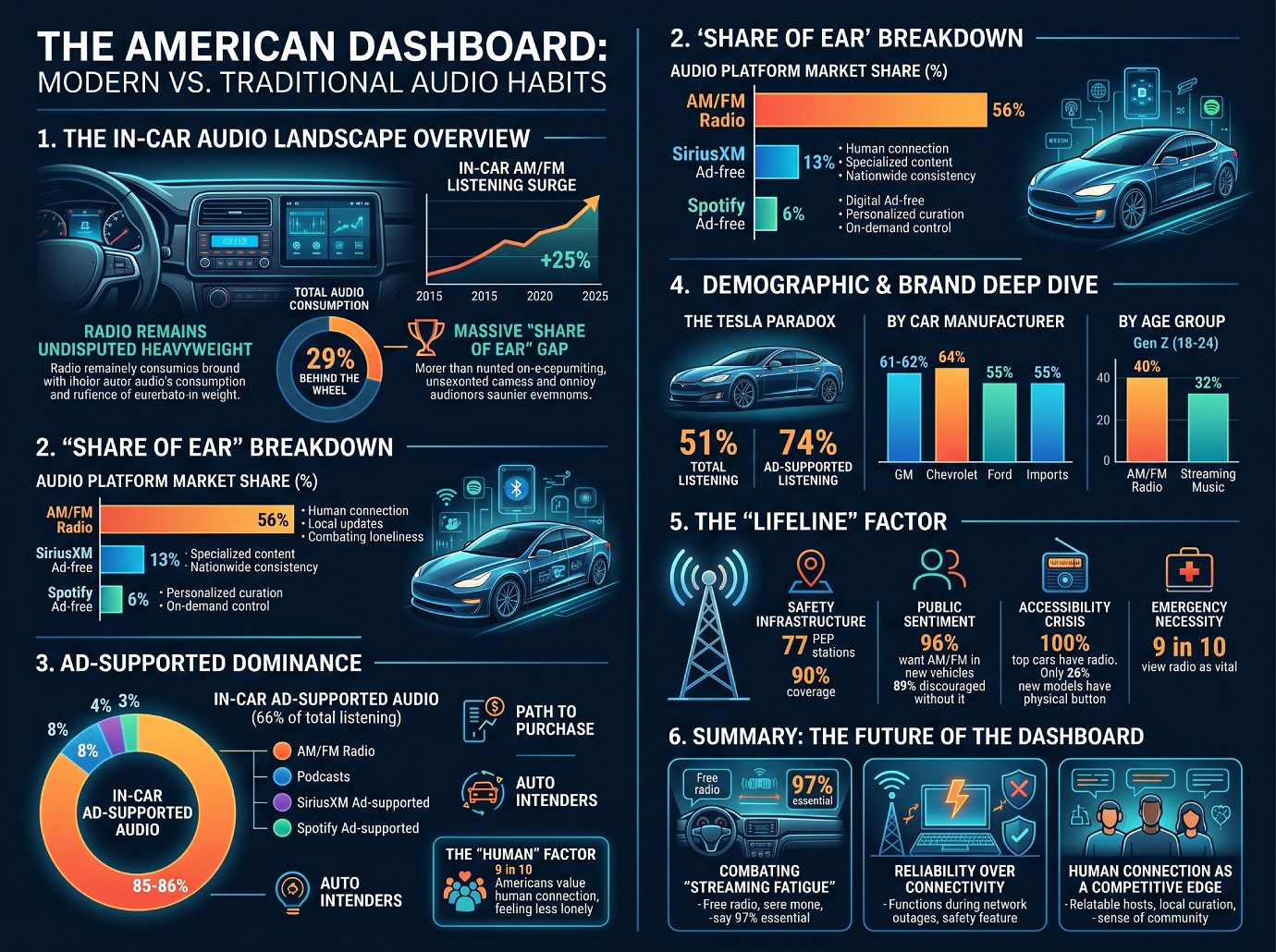

Fact Sheet: The American Dashboard—Modern vs. Traditional Audio Habits

Fact Sheet: The American Dashboard—Modern vs. Traditional Audio Habits

1. The In-Car Audio Landscape: An Overview

The narrative surrounding the “death of radio” is not just premature—it is demonstrably false. As a Learning Architect and Strategist, it is vital to recognize that the American dashboard has become a growth engine for traditional media. Far from declining, the proportion of AM/FM radio listening occurring in the car has surged by 25% since 2015. In-car audio consumption has rebounded past pre-pandemic levels, proving that terrestrial radio remains the undisputed heavyweight of the daily commute, despite the proliferation of digital infotainment systems.

Key Insight: The vehicle is the primary battleground for audio platforms, with 29% of all total audio consumption occurring behind the wheel.

This landscape is defined by a massive “Share of Ear” gap that modern competitors have yet to bridge, underpinned by deep-seated consumer habits and psychological needs.

2. The “Share of Ear” Breakdown: Platforms by the Numbers

Data from the Edison Research Q2 2025 “Share of Ear” study highlights the significant dominance of broadcast radio over modern subscription and streaming services. While digital integration via CarPlay or Android Auto is present in many vehicles—reaching 55% of drivers through online audio—drivers consistently prioritize the broadcast experience.

| Audio Platform | Market Share (%) | Primary Consumer Benefit |

|---|---|---|

| AM/FM Radio | 56% | Human connection, local updates, and combating loneliness. |

| SiriusXM (Ad-free) | 13% | Specialized content and nationwide consistency. |

| Spotify (Ad-free) | 6% | Personalized curation and on-demand control. |

While these figures represent total market share, the competitive gap widens even more dramatically when we isolate the advertising-supported market, where brands actually reach their audience.

3. Ad-Supported Dominance: Where Brands Connect

In the car, 66% of all audio listening is ad-supported, and AM/FM radio is the “Queen of the Road” in this category. It commands a staggering 85–86% share of all ad-supported minutes, leaving digital competitors in the proverbial rearview mirror.

- Unrivaled Scale of Dominance: AM/FM’s share is nearly ten times larger than its nearest ad-supported competitor. While others are growing, the breakdown reveals a massive drop-off: Podcasts (8%), SiriusXM ad-supported (4%), and Spotify ad-supported (3%).

- The “Auto Intender” Advantage: Radio reaches consumers on the “path to purchase.” Because listeners are reached while driving, marketers have a unique strategic advantage in influencing “auto intenders” and retail shoppers immediately before they reach a point of sale.

- The “Human” Factor in Reach: Nine in ten Americans value the human connection of radio. Listeners report that relatable on-air personalities help them “feel less lonely,” a psychological hook that automated streaming playlists cannot replicate.

This dominance is not limited to older demographics; it persists across car manufacturers and even among the most tech-forward listeners.

4. Demographic & Brand Deep Dive: Surprising Loyalties

Loyalty to broadcast radio remains high across all vehicle types, including high-tech electric vehicles. This is most evident in the “Tesla Paradox.”

- The Tesla Paradox: Despite Tesla removing AM tuners in some models, AM/FM still captures 51% of total listening time among Tesla owners. More crucially, in the ad-supported category, Tesla drivers give a massive 74% of their time to AM/FM, proving that even tech-forward drivers prefer radio when they aren’t paying for a subscription.

- By Car Manufacturer: AM/FM remains the dominant audio source for all major brands:

- General Motors (GM): 61–62% share of in-car audio.

- Chevrolet: 64% share.

- Ford: 55% share.

- Import Brands: 55% share (including Toyota, Honda, and Subaru).

- By Age Group: Younger listeners show a surprising “soft spot” for radio. In the Gen Z (18–24) demographic, AM/FM radio captures 40% of listening, significantly outperforming streaming music services at 32%.

5. The “Lifeline” Factor: Consumer Demand & Public Safety

The conversation has shifted from radio as a “luxury” feature to radio as a “lifeline.” The bipartisan support for the “AM Radio for Every Vehicle Act” is fueled by the reality that radio is the backbone of the Emergency Alert System.

Fact File: The Vital Necessity of Radio

- Safety Infrastructure: 77 Primary Entry Point (PEP) stations, a majority of which are AM, cover 90% of the population and remain functional when cell towers and internet fail.

- Public Sentiment: 96% of Americans want AM/FM radio in new vehicles; 89% would be discouraged from buying a car without it.

- The Accessibility Crisis: While 100% of top-selling cars include radio, only 26% of new models feature a physical radio button (down from 36% in 2024), creating a tension between consumer necessity and infotainment design.

- Emergency Necessity: 9 in 10 respondents view radio as vital for emergency information.

6. Summary: The Future of the Dashboard

Traditional audio remains the enduring presence in the vehicle because it satisfies human needs for simplicity, community, and security that digital platforms struggle to match.

3 Takeaways for the Future

- Combating “Streaming Fatigue”: With 97% of consumers viewing free entertainment as essential, the shift away from paid, fragmented digital subscriptions back to “free radio” is a growing market driver.

- Reliability Over Connectivity: As the only medium that functions during total network outages, radio is being redefined as a standard safety feature rather than an entertainment option.

- Human Connection as a Competitive Edge: Radio’s success is rooted in the “Human Consumer” trend. Relatable hosts and local curation provide a sense of community that makes the American dashboard a “strategic battleground” where radio remains the incumbent power.

——————————————————————————–

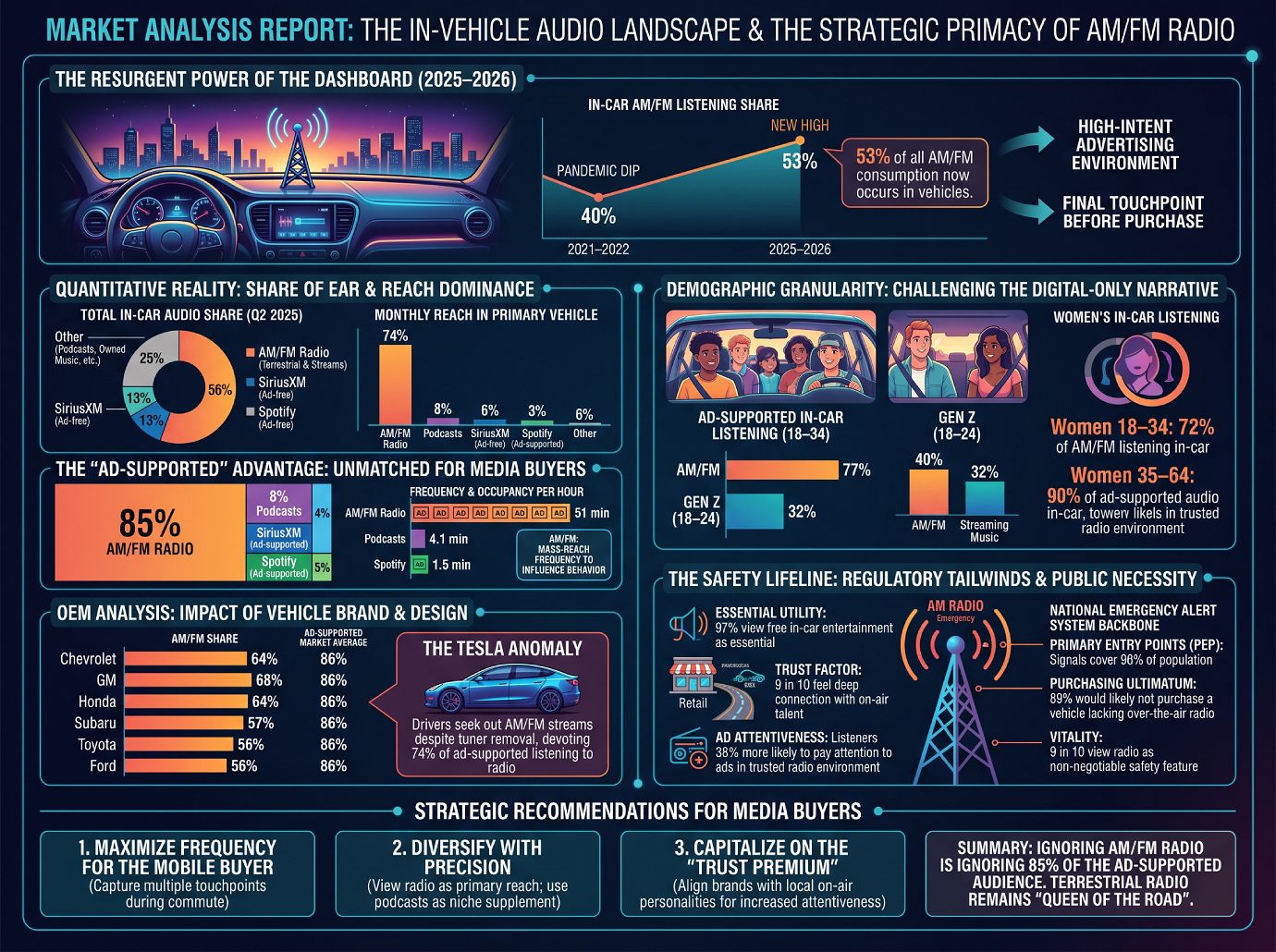

Market Analysis Report: The In-Vehicle Audio Landscape and the Strategic Primacy of AM/FM Radio

Market Analysis Report: The In-Vehicle Audio Landscape and the Strategic Primacy of AM/FM Radio

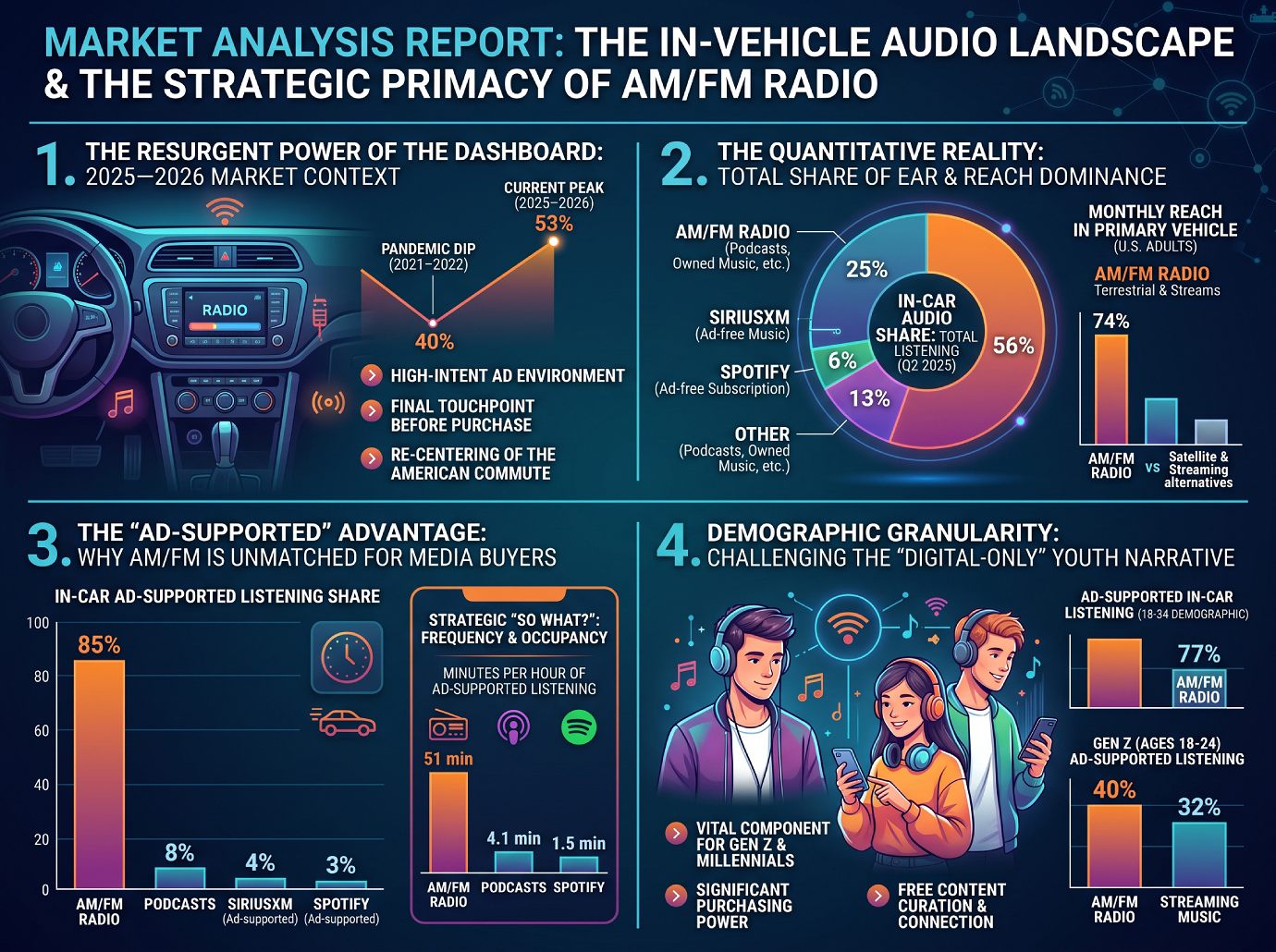

1. The Resurgent Power of the Dashboard: 2025–2026 Market Context

In the high-stakes arena of media mix optimization, the vehicle remains a uniquely high-intent advertising environment. For brands targeting “auto intenders” and mobile consumers, the dashboard represents the final, unencumbered touchpoint before a point-of-purchase decision. As we enter the 2025–2026 cycle, the strategic importance of this space has been reaffirmed by a significant rebound in in-car listening. Current data indicates that 53% of all AM/FM radio consumption now occurs in vehicles—a new high that re-establishes the dashboard as the primary battleground for consumer attention.

This resurgence marks a definitive shift from the “pandemic dip” observed during 2021–2022. During that period, the share of in-car AM/FM consumption plummeted to a low of 40% as commuting patterns were disrupted. The climb back to the current 53% peak signals more than just a return to the office; it indicates a re-centering of the American commute as a critical window for reaching a captive audience. For strategists, the “so what” is undeniable: the vehicle is the command center of the mobile path to purchase, necessitating a quantitative breakdown of where actual consumer time-spend is directed.

2. The Quantitative Reality: Total Share of Ear and Reach Dominance

To evaluate the true efficacy of audio platforms, media strategists utilize “Share of Ear” data as the gold standard for measuring real-world consumer time-spend. While digital platforms frequently tout availability or “downloads,” market dominance is defined by active selection—where consumers choose to spend their minutes while behind the wheel.

The data reveals that reach is not merely a matter of a platform being present in the interface, but of being the default choice for the American driver. The following table illustrates the distribution of total listening time across all tiers.

In-Car Audio Share: AM/FM vs. Competitors (Q2 2025)

| Audio Platform | Total Share of In-Car Listening (Ad-supported & Ad-free) |

|---|---|

| AM/FM Radio (Terrestrial & Streams) | 56% |

| SiriusXM (Ad-free Music Channels) | 13% |

| Spotify (Ad-free Subscription) | 6% |

| Other (Podcasts, Owned Music, etc.) | 25% |

The “reach gap” remains the most significant hurdle for digital-only competitors. Approximately 74% of U.S. adults tune into AM/FM radio in their primary vehicle monthly, effectively dwarfing satellite and streaming alternatives. While subscription services have secured a foothold, they remain secondary to the massive, consistent reach of over-the-air broadcasts. This disparity is further magnified when the lens is shifted to the metrics that matter most to media buyers: the ad-supported environment.

3. The “Ad-Supported” Advantage: Why AM/FM is Unmatched for Media Buyers

For advertising strategists, the critical distinction lies between “total listening” and “ad-supported listening.” While a platform like Spotify maintains a notable presence, the vast majority of its in-car usage is locked behind ad-free premium firewalls, rendering it invisible to traditional brand campaigns. AM/FM radio, conversely, remains the primary engine for en masse reach.

In the ad-supported category, AM/FM radio maintains a crushing dominance over all other platforms:

- AM/FM Radio: 85%

- Podcasts: 8%

- SiriusXM (Ad-supported tiers): 4%

- Spotify (Ad-supported tiers): 3%

The Strategic “So What?”: Frequency and Occupancy This dominance translates into a massive frequency advantage. Within a typical hour of ad-supported in-car listening, consumers spend approximately 51 minutes with AM/FM radio, compared to just 4.1 minutes for podcasts and 1.5 minutes for ad-supported Spotify. In a standard 20-minute commute, an AM/FM listener will likely be exposed to multiple ad touchpoints across several breaks. In contrast, a podcast listener may hear only a single “pre-roll” or potentially zero ads if the episode exceeds the commute length. For media buyers, AM/FM is the only medium capable of delivering the mass-reach frequency required to influence immediate consumer behavior.

4. Demographic Granularity: Challenging the “Digital-Only” Youth Narrative

A persistent misconception in the industry is that younger audiences have abandoned terrestrial radio. However, the 2025 data challenges this “digital-only” narrative, revealing that AM/FM remains a vital component of the media mix for Gen Z and Millennials—groups with significant and growing purchasing power.

Among the 18–34 demographic, AM/FM radio commands 77% of all ad-supported in-car audio listening. Even more striking is the data for the youngest cohort: Gen Z (ages 18–24) consumes more ad-supported radio (40%) than streaming music (32%). These listeners gravitate toward radio for free content curation and a sense of connection that algorithms cannot replicate.

Demographic analysis also highlights the “astonishingly high” proportion of in-car listening among women:

- Women 18–34: 72% of all their AM/FM radio listening occurs within the vehicle.

- Women 35–64: This demographic hits an even higher concentration, with 90% of their ad-supported audio time spent with AM/FM radio while driving.

5. OEM Analysis: Impact of Vehicle Brand and Design on Audio Selection

The relationship between vehicle hardware (OEM infotainment systems) and listener software (consumer choice) is a primary factor in maintaining audio dominance. While some manufacturers have experimented with removing traditional tuners, consumer behavior across major brands remains remarkably stable.

AM/FM Share of Total In-Car Audio by Brand

| Vehicle Brand | AM/FM Share of Total In-Car Listening | Ad-Supported Market Average |

|---|---|---|

| Chevrolet | 64% | 86% |

| General Motors Group | 60.7% | 86% |

| Honda | 62% | 86% |

| Subaru | 60% | 86% |

| Toyota | 56% | 86% |

| Ford | 55% | 86% |

The Tesla Escalation and Consumer Persistence Tesla represents a critical case study in the tension between OEM design and consumer demand. Tesla has moved to remove not just AM, but also FM tuners from certain low-cost models. This is a strategic risk that overlooks the “Tesla Anomaly”: despite tuner removal, Tesla drivers still devote 74% of their ad-supported listening to AM/FM radio, seeking out the content via digital streams. This persistence proves that drivers view radio content—local news, personalities, and free music—as non-negotiable, even when the hardware forces them to seek alternative access points.

6. The “Path to Purchase” and Consumer Sentiment

The “mobile path to purchase” is the window in which a consumer is most receptive to retail, automotive, and Quick Service Restaurant (QSR) messaging. Pierre Bouvard of Cumulus Media describes radio as the “soundtrack of the American worker,” highlighting its role in influencing decisions immediately before a purchase is made.

Findings from Critical Mass Insights suggest that “streaming fatigue” is driving a return to the simplicity of radio:

- Essential Utility: 97% of Americans view free in-car entertainment as essential; 96% would “miss” radio if it were removed.

- The Trust Factor: 9 in 10 listeners feel a deep connection with on-air talent. This “human connection” makes radio a “trusted” medium, which directly influences the bottom line: listeners are 38% more likely to pay attention to ads in this environment compared to non-trusted digital platforms.

7. The Safety Lifeline: Regulatory Tailwinds and Public Necessity

Beyond its commercial dominance, AM radio serves as the backbone of the National Emergency Alert System. The “AM Radio for Every Vehicle Act” serves as a market stabilizer for advertisers, ensuring radio remains a standard feature.

Public sentiment regarding safety is an overwhelming force that OEMs ignore at their peril:

- Primary Entry Points (PEP): There are 77 PEP stations across the U.S. whose signals cover 90% of the population. These stations have direct links to FEMA, ensuring they stay on-air when cell towers and internet services fail.

- The Purchasing Ultimatum: 89% of consumers state they would likely not purchase a vehicle that lacks an over-the-air radio.

- Vitality: 9 in 10 respondents view radio access as a non-negotiable safety feature for emergencies and natural disasters.

8. Strategic Recommendations for Media Buyers and Strategists

The 2025–2026 data confirms that AM/FM radio is a resurgent, dominant force. For media planners, excluding this medium is not just a missed opportunity—it is strategic malpractice. To optimize for the current landscape, buyers must adopt three mandates:

- Maximize Frequency for the Mobile Buyer: Leverage radio’s 85% ad-supported share to capture multiple touchpoints during a single commute. With 51 minutes of occupancy per hour, radio provides the “frequency-of-touchpoint” that podcasts and streaming cannot match.

- Diversify with Precision: View radio as the primary reach vehicle. Use podcasts (8% share) as a niche tactical supplement for deep-dive engagement, but do not mistake them for a mass-reach replacement.

- Capitalize on the “Trust Premium”: Align brands with local on-air personalities. The human connection reported by 90% of listeners creates a trusted environment that increases ad attentiveness by 38%, a metric digital algorithms cannot replicate.

Summary: In the 2025–2026 media environment, ignoring AM/FM radio in an in-vehicle campaign is a deliberate choice to ignore 85% of the available ad-supported audience. Terrestrial radio remains the “Queen of the Road” and the most efficient engine for driving mass-market brand equity and retail conversion.